Brasil: Cenário Macroeconômico

|

|

|

- Martim Bergler de Carvalho

- 8 Há anos

- Visualizações:

Transcrição

1 Brasil: Cenário Macroeconômico Maio 2015 Gilson Carvalho Fiat Chrysler Finanças

2 Indicadores Macroeconômicos Atividade P 2016P PIB (USD bilhões) PIB (BRL bilhões) PIB (%) 7,6 3,9 1,8 2,7 0,1 (1,4) 0,9 Credito (BRL bilhões) Credito (% PIB) 44,1 46,5 50,3 52,6 54,7 56,8 58,1 População (milhões) ,2 205,7 PIB per capta (USD) Taxa de Desemprego (%) 6,7 6,0 5,5 5,4 4,8 6,4 7,4 Contas Externas P 2016P Balança Comercial (USD bilhões) 20,1 29,8 19,4 2,6 (3,9) 0,7 9,6 Balança em Conta Corrente (USD bilhões) (47,4) (52,5) (54,2) (81,1) (90,9) (82,5) (75,6) Balança em Conta Corrente (% PIB) (2,1) (2,0) (2,2) (3,4) (3,9) (4,1) (3,9) Investimento Estrangeiro Direto (USD bilhões) 48,4 66,7 65,3 64,0 62,5 45,0 50,0 Reservas Internacionais (USD bilhões) 287,9 352,0 378,6 375,8 374,1 365,6 361,5 Dívida Externa Total (USD bilhões) 255,7 298,2 316,8 312,0 347,6 378,2 409,2 Contas Públicas P 2016P Superávit Primário (% PIB) 2,6 2,9 2,2 1,8 (0,6) 0,9 1,8 Meta Superávit Primário (% PIB) 2,2 2,3 2,2 1,9 1,8 1,2 2,0 Câmbio, Juros e Inflação P 2016P Taxa de Juros (Selic - final de período) 10,75 11,00 7,25 10,00 11,75 13,75 12,00 Inflação (IPCA, %) 5,9 6,5 5,8 5,9 6,4 8,4 5,5 BRL/USD (final de período) 1,67 1,88 2,04 2,34 2,66 3,2 3,3 As série de contas externas não consideram a metodologia adotada pelo Bacen a partir de abril Source: Market Consensus, FCF 2

6,7 6,0 5,5 5,4 4,8 6,4 7,4 Contas Externas 2010 2011 2012 2013 2014 2015P 2016P Balança Comercial (USD bilhões) 20,1 29,8 19,4 2,6 (3,9) 0,7 9,6 Balança em Conta Corrente")

3 Cenário Macroeconômico 1. Fraco desempenho do crescimento em meio a um aumento dos desequilíbrios macro econômicos Recessão em 2015 Crescimento abaixo de 1% em 2016 Demanda doméstica fraca Investigação de corrupção da Petrobras Deterioração do mercado de trabalho Diminuição do crescimento de crédito Inflação elevada 2. Desafios fiscais Déficit fiscal elevado Aumento do gasto do governo Riscos para consolidação fiscal (contração econômica; atraso na implementação das medidas fiscais) 3. Cenário político complicado Perda de popularidade da presidente Congresso fragmentado Investigação de corrupção da Petrobras Fatores de risco para rebaixamento do grau de investimento Continuação do fraco desempenho de crescimento Dificuldade na consolidação fiscal Baixa confiança no processo de implementação das medidas de ajuste fiscal Perda de reservas internacionais Pontos a serem monitorados Contas fiscais indicadores de confiança Eficácia congelamento dos gastos do governo Êxito das de medidas fiscais no Legislativo Fatores fundamentais para melhorar o cenário macro Melhoria da credibilidade política Redução dos desequilíbrios macro econômicos Consolidação fiscal Melhor ambiente de investimento 3

3.")

4 Cenário Macroecônomico Nível de Atividade: Brasil apresenta fraco desempenho do crescimento em meio aos desequilíbrios macroeconômicos, com previsão de crescimento abaixo de 1% em 2016, dificuldade de acesso ao crédito, fraca demanda doméstica e deterioração do mercado de trabalho Inflação: Pressão sobre os preços administrados, desvalorização do real e aumento dos impostos apontam para elevada inflação em 2015, acima do teto da meta de 6,5% Juros: Na última reunião o COPOM aumentou a Selic em 0,5% pp e sinalizou que apesar de próximo o fim do ciclo de aperto monetário não será na próxima reunião Câmbio: O real já depreciou em mais de 15% nesse ano com forte volatilidade e bastante sensível às incertezas políticas, apesar disso o BC não prorrogou o programa de swaps. Balança Comercial: A balança comercial permanece fraca e já acumula um déficit de USD 5 bi até abril. IED: A grande diferença das taxas de juros locais e internacionais contribuem para o influxo de capital estrangeiro no país, apesar da instabilidade política e recessão econômica pela qual o país está passando 4

5 Cenário Macroeconomico Crédito: a pífia performance econômica, a deterioração do mercado de trabalho e os baixos índices de confiança do consumidor e empresário contribuem para a redução do crédito tanto para as empresas quanto para pessoa física Contas Publicas: apesar do comprometimento do governos com a meta fiscal, o país tem desafios adiante, pois precisa superar a contração econômica, a dificuldade em cortas os gastos e a perda das reservas internacionais além da incerteza na aprovação das medidas de ajuste fiscal Politica: o cenário político está ainda mais instável devido a perda de popularidade da presidente, a fragmentação do congresso e a investigação de corrupção da Petrobrás Risco Soberano: o risco de um rebaixamento do grau de investimento é real. As agências de rating estão monitorando a consolidação fiscal, a deterioração dos índices de confiança e o êxito das medidas fiscais no Legislativo A retomada do crescimento em 2016 (e manutenção da classificação de grau de investimento) depende da extensão dos ajustes implementados em

6 Backup

7 GDP 7

8 Activity Level 2014 GDP growth was 0.1% better than forecasted, but already incorporated in the new methodology... The perspective for 2015 is one of the worst regarding GDP. The market already expects -1.4%. The last GDP data was released in March by IBGE according to the new methodology for National Accounts. IBGE also revised the historical series using the new methodology. The most relevant changes occurred between 2011 and 2013, with an upward revision in the growth rates. 7,6% GDP 3,9% GDP 2014 (bn): BRL 5,521 2,7% 1,8% 0,1% 0,9% -1,4% F 2016F Source: IBGE, FCF 1/9 8

9 Activity Level A bunch of reasons explain Brazilian s low growth Punctual Issues Structural Issues Domestic Issues Global Issues Infrastructure Investments High inflation Low credibility on fiscal policy Reduced predictability Risk of electricity and water rationing Downgrade rating Petrobras Low growth on important markets (Euro Area) China s growth slowdown Risk of Greece leaving Euro Area Low business and consumer confidence Poor infrastructure conditions impact productivity Demography Lost of momentum of labor force Low productivity Reduced Cross Border Trade High raw material import taxes and few commercial agreements with non prime counterparties Fragility of Institutions Poor perception over quality of institutions Negative GDP Growth Potential growth lower than 3,0% Source: Credit Suisse, BofA, FCF 2/9 9

10 Purchasing Managers Index (PMI) The Markit manufacturing Purchasing Managers Index (PMI) fell from March s 46.2 to 46.0 in April, thus dropping to the lowest level in over four years. As a result, the PMI index is now further below the 50-threshold that separates contraction from expansion in business conditions in the manufacturing sector. According to Markit, April s figure came on the back of a steeper decrease in output, new business and buying levels. PMI Note: A reading above 50 indicates an expansion in business activity while a value below 50 points to a contraction. Source: Latin Focus 3/9 10

11 Labor Market Deterioration in labor market conditions in 2015 is expected. The growth of occupied population will be compatible with the slight increase in the unemployment rate in next years. Source: BCB, FCF 4/9 11

12 Mar-10 May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 Unemployment UNEMPLOYMENT INDEX FEAR OF UNEMPLOYMENT INDEX 98,8 74, ,8 72,2 74,4 74,6 71,6 76,5 73,5 74,7 75,3 74, ,3 72, ,6 76, /9 Source: IBGE & CNI 12

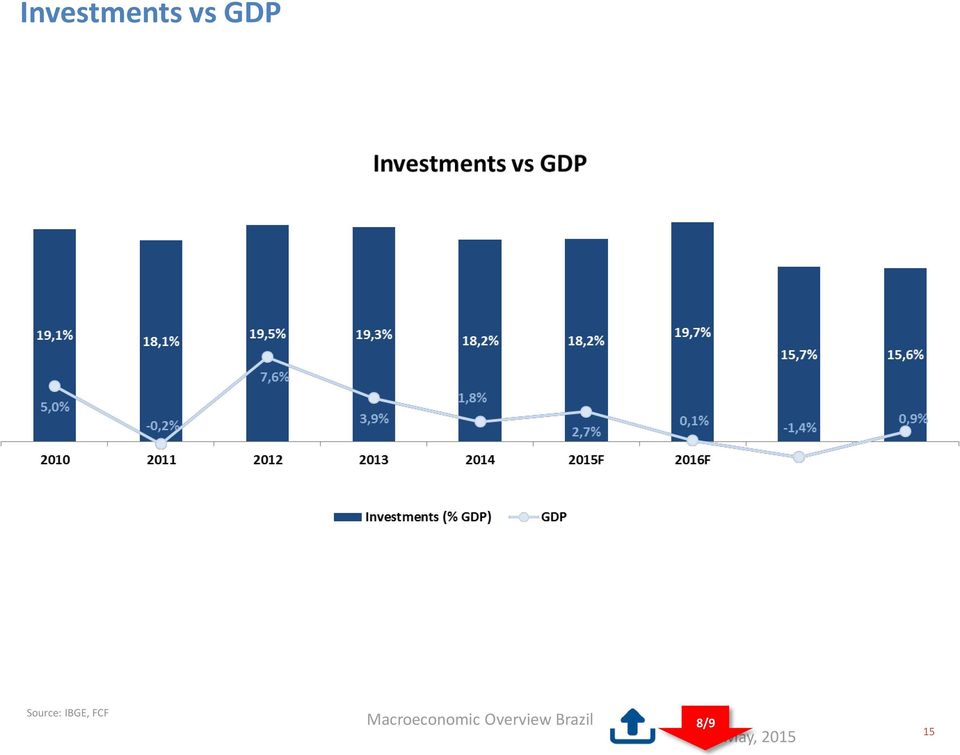

13 GDP Breakdown Increase of Brazilian GDP s growth depends on a substantial hike in investments rate and on some internal measures (labor reform, tax reform, enhancements on infrastructure) and a better global outlook... Breakdown of GDP value added in 2014 (%) 5,6-14,3% 23,4 11,6% 62,7% 19,8% 71,0 20,3% Agriculture Industry Services Household Consumption Government Consumption Investments Exports Imports...The low level of confidence indexes (business and consumers) led to a investments deceleration in Source: IBGE, Tendências, FCF 6/9 13

14 Supply Demand GDP Breakdown On the demand side, the decrease in the investments and the fall in imports explained the lower GDP growth during F 2016F Household Consumption 6,4% 4,2% 6,4% 4,8% 3,9% 2,9% 0,9% 0,2% 0,1% Government Consumption 2,1% 2,9% 3,9% 2,2% 3,2% 2,2% 1,3% 2,2% 2,0% GDP (%) GDP growth on supply and demand sides (%) Investments 12,7% -1,9% 17,8% 6,6% -0,6% 6,1% -4,4% -4,6% 0,6% Exports 0,4% -9,2% 11,7% 4,8% 0,5% 2,1% -1,1% -1,4% 5,0% Imports 17,0% -7,6% 33,6% 9,4% 0,7% 7,5% -1,0% -9,0% -3,7% Agriculture 5,5% -3,8% 6,8% 5,6% -2,5% 7,9% 0,4% 0,1% 0,9% Industry 3,9% -4,8% 10,4% 4,1% 0,1% 1,8% -1,2% -4,3% 2,3% Services 4,8% 1,9% 5,8% 3,4% 2,4% 2,5% 0,7% -0,7% 1,0% 5,0% -0,2% 7,6% 3,9% 1,8% 2,7% 0,1% -1,4% 0,9%...On the supply side, industry and agriculture reverted the strong increase presented in Source: IBGE, Tendências, FCF 7/9 14

15 Investments vs GDP Source: IBGE, FCF 8/9 15

16 Investments vs GDP Lack of suitable infrastructure is a serious bottleneck to increase growth pace of Brazil. Investment rate of Brazil is recurrently lower than 20%. Infrastructure investments are far below the level of other developed countries and from BRICS. Infrastructure Investments in Brazil (% of GDP) China Japan India Other Developed Countries Middle East & Africa Infrastructure Investments (% of GDP, average ) Eastern Europe European Union USA LatAm Brazil Water Energy Airports Ports Railroads Highways Source: BNDES, Credit Suisse 9/9 16

China Japan India Other Developed Countries Middle East & Africa Infrastructure Investments")

17 Inflation 17

18 Inflation CPI began the year upper the limit of 6.5% yoy and should keep pressured along 2015, mainly due to administered prices and food... CPI Evolution (% p.y) 8,4 5,9 6,5 5,8 5,9 6,4 5,5 4,3 4,5 4,5 4,5 4,5 4,5 4,5 4,5 4,5 CPI Target F 2016F besides the inflation will be above the upper target limit in the current year, the government has been taken the measures to bring the inflation closer to the target in Source: IBGE, FCF 1/ 1 18

19 Interest Rates & FX 19

20 Interest Rates At last Central Bank Monetary Policy Committee (COPOM) meeting, Selic was raised in another 50 bp to 13.25% in May 2015 that until now bring a +600 tightening cycle initiated in April 13. Market expects another hike of 50bp to reach 13.75% in the end of There are few entities in the market that are forecasting a Selic at 14% in the end of this year. Interest Rate - Selic (% p.y.) 13, ,50 12, ,00 11,00 12,00 9 8,75 7,25 7 Besides the pressured inflation, it should remain high along the year since the focus of the monetary authority moves to 2016, the monetary policy strategy tends to put less weight on current inflation and more attention on economic growth and fiscal adjustment. Source: BCB, FCF 1/ May,

21 FX Since the middle of 2011, BRL entered in a downward trend. From September 2014 until now the deterioration of fiscal accounts, the uncertainty about economic policy to be adopted, the turbulences around political environment and the difficulty on the fiscal adjustment approval led to a sharp deterioration in the flow to Brazil and the exchange rate had depreciated faster. The market expects BRL 3.20 / USD for the end of Source: BCB, FFB 1/ May,

22 FX BRL x USD : Currency behavior in the last years FHC FHC Lula Lula Dilma PSDB x PT 54,28 x 27,04 PSDB x PT 53,06 x 31,01 PT x PSDB 46,44 x 23,19 PT x PSDB 48,61 x 41,64 PT x PSDB 46,91 x 32,61 PT x PSDB 51,6 x 48,4 Source: BCB, TSE, FFB 2/ May,

23 External Accounts 23

24 Trade Balance The first annual deficit since 2000, 2014 posted a trade balance deficit of USD 3.9 bn 50% 40% 30% 20% 10% 0% -10% -20% -30% 32% 44% 46,1 42% 44,7 32% 40,0 32% 30% 27% 25% 33,7 23% 24% 23% 29,8 17% 16% 17% 24,7 25,3 20,3 7% 19,4 3% 0% 9,6-1% -5% -4% -2% -7% 2,6 0,7 (3,9) -16%-18% -23% -26% F 2016F Exports (%) Imports (%) Trade Balance (USD bi) 50,0 40,0 30,0 20,0 10,0 - (10,0)...Mainly explained by the contraction of exports, that negatively affected commodity prices and the slowdown in demand of major trading partners. As séries de contas externas não consideram a metodologia adotada pelo Bacen a partir de abril Source: Market Consensus/BCB, MDIC, FCF 1/ May,

25 Trade Balance 2014 Main Products Main Exported Products 2014 Main Imported Products 2014 Main Exported Products Value % Share 1 - Soybeans & products Ores ,6 3 - Oil and fuel ,2 4 - Transport material ,1 5 - Meats ,5 6 - Chemicals ,7 7 - Metallurgic products ,4 8 - Sugar & ethanol ,6 9 - Machines & equipaments , Paper & pulp , Coffee , Footwear & leather , Eletric equipament , Precious metals and stones , Textiles ,1 Main Imported Products Value % Share 1 - Fuel and Oil ,7 2 - Mechanical Equipment ,9 3 - Electrical and Electronical Equipment ,8 4 - Motor Vehicles and parts ,5 5 - Organic and Inorganic Chemicals ,6 6 - Plastics and its Products ,9 7 - Fertilizers ,7 8 - Iron, Steel and its Products ,3 9 - Pharmaceutica , Optical and Precision Equipment Rubber and its products , Cereals and milling products , Airplanes and its parts , Synthetic and Arificial Filaments and Fibers , Cooper and its products ,9 Source: Secex, Mdic 2/ May,

26 Current Account The current-account deficit was the widest in 13 years. The deficit is boosted by the trade balance deficit. Current- Account Balance ,8 1,6 1,3 2 1, , , ,5-1, ,7-1,5-2,1-2 -2,2-2, , ,5-4 -4,3-3,8-4,2-3, ,9-4,0-3,9-4,5 This deficit was funded mostly by a higher volume of external loans, which drove the external debt up. Source: BCB, Credit Suisse, FCF USD billion As séries de contas externas não consideram a metodologia adotada pelo Bacen a partir de abril % of GDP 3/ May,

27 Foreign Direct Investments (FDI) Foreign direct investments (FDI) are expected to decline in the upcoming years as a result of lower growth perspectives for the local economy Intercompany Loans Capital market share As séries de contas externas não consideram a metodologia adotada pelo Bacen a partir de abril Source: BCB, FCF 1/ May,

28 Credit Operations 28

29 Credit x Income Commitment x Delinquency The population leverage has become much bigger in recent years, with no room for new financial loans. According to the current scenario, interest rates have gone up and credit costs are higher nowadays. 70,0 60,0 Credit Operations (%GDP) Income Commitment (%) Delinquency Rate for Individuals (%) 50,3 52,6 54,7 56,8 58,1 50,0 40,7 43,9 44,1 46,5 40,0 35,5 30,0 31,3 30,2 20,0 17,4 18,2 18,2 18,9 19,6 19,7 23,3 22,9 21,9 22,0 22,0 21,8 10,0 6,2 6,9 6,4 7,2 7,0 5,3 6,7 6,9 5,7 6,8 5,4 5, F 2016F Source: BCB, FCF 1/ May,

30 Delinquency Delinquency remained relatively stable in 2014 following the reduction in credit concessions to auto financing. Total loans to this segment decreased 4.5% in 2014, leading delinquencies to decline from 5.2% to 3.9%. Delinquency Rate (%) The rising unemployment, low confidence, and tightened monetary and fiscal policies, creates an expectation that credit growth continue its gradual deceleration and delinquency tends to increase, as it adjusts to a challenging economic scenario for companies and consumers. Source: BCB, Credit Suisse 2/ May,

31 Credit Operations As a result of the current monetary tightening cycle, spreads and interest rates also increased in the period for both earmarked and non-earmarked operations. Total Credit Operations (% GDP) 43,9 44,1 46,5 50,3 52,6 54,7 56,8 58, F 2016F Based on the scenario for economic activity in the current year, the continuity of monetary politic and the ongoing fiscal adjustment, the deceleration in credit operations is expected. Source: Market Consensus/BCB, FCF 3/ May,

32 BNDES participation Since 2008, National Treasury injected more than BRL 400 bln in the Public Banks to support credit originations and offset the effects of financial crisis No further contribution from National Treasury to public banks in the next 3 years, due to the high impact on public accounts, with reflects over sovereign credit ratings Track Record of Money Injection on Public Banks (BRL bln) Source: BNDES, Credit Suisse, FCF 4/ May,

33 TJLP x Selic Current tightening cycle (initiated on October 2014) widened the gap between Selic and TJLP ( Long Term Interest Rates ) to 625 bps (biggest gap since 2008). In the last week of December, CMN announced an increase of TJLP to 5,50%py. Market currently predicts further increases on TJLP along 2015, so that it will surpass 6,00%py level at year end. Source: BNDES, FCF 5/ May,

34 Bank loans Participation of public on total credit portfolio increased from 34% in 2007 to 59% on December Origination pace of credit operations at public banks decreased from 11.2% yoy to 10.5% yoy in April, totaling BRL trillion, which represents 54.5% of GDP. Source: Credit Suisse, FCF 6/ May,

35 Public Accounts 35

36 Public Accounts Fiscal account has deteriorated very sharply since 2011 at both the flow (fiscal deficit) and stock (gross public debt) levels. The consolidated public sector recorded a primary deficit of 0.6% of GDP in 2014 as a direct result of lower tax revenues for the central government due to less contributions related to a smaller economic growth and an increased in the government expenditure. Brazilian Debt (% GDP) 60,9 53,4 54,2 58,7 57,2 58,9 61,7 61,9 42,1 39,2 36,4 35,2 33,8 34,1 35,0 41, F 2016F Net Debt Gross Debt Gross debt has increased owing to the continued direct issuance of BRL 60.0 billion to the BNDES and a fiscal deficit (primary surplus minus interest payment) of 6.7% of GDP. The steady erosion of the fiscal stance pushed net and gross public debt up. Net debt is gross debt minus financial assets corresponding to debt instruments. These financial assets are: monetary gold and SDRs, currency and deposits, debt securities, loans, insurance, pension, and standardize guarantee schemes and other accounts receivable. Source: Market Consensus /BCB, FCF 1/ 5 36

37 Primary & Nominal Results The primary result posted a deficit of 0.6% of GDP in The cumulative primary surplus in 2015 has reached 28% of the objective set for the year (1.2% of GDP). Recession will make it an even more challenging goal for the year, and Central Bank already admits it. The market expects a primary surplus of 0.9% of GDP in For 2016, the forecasted target is 2.0% of GDP. Public Sector Primary Result Source: Credit Suisse, FCF 2/ May,

38 Fiscal Measures Source: Santander, FCF Before Wage bonus Needs 1 month of work Needs 6 months working Unemployment insurance Needs 1 month of work Needs 18 months working for 1st request ( 12 months for the 2nd request and 6 months for the 3rd) Death pension Pay the total amount (w/o limits) Needs 2yrs married and 2yrs of contribution to the pension system. Payment depend on the age expectancy: 50% of the total amount is paid. Young widow(er) will not receive Unemployment insurance to fishermen When it is not fishing season 3yrs as fisherman needed and cannot receive this benefit if receives another (as illness assistance) Sick leave as of 15 days out of work due to illness As of 30 days out of work due to illness ( 12 months for the 2nd request and 6 months for the 3rd) None CIDE at gasoline and diesel prices/ CIDE and PIS/Cofins (tax on gasoline and CIDE at 10 cents in gasoline price and 5 cents in diesel price/ PIS/Cofins at PIS/Cofins at BRL0.266 cents in gasoline price diesel) 12 cents in gasoline and at 10 cents in diesel prices and at BRL0.148 cents in diesel price IPI (tax on cars production) 3% - 9% 7% - 13% IPI (tax on cosmetics) Wholesale prices equalized to retail prices IOF (tax on finacial operations) on consumer 1.50% loans 3% PIS/Cofins on imports 9.25% 11.75% PIS/Cofins on financial revenues 0% 4.65% FIES (government funded scholarship Extended the period to fulfill its obligations with the private schools on the program) program, reducing its short term monthly Financial institution's Social Contribution on 15% Net Income (CSLL) 20% 2015 Budget Government will freeze BRL 69.9 billion reais (USD22.5 billion) of spending from 2015 budget. In January the Government has reinforced its commitment to fiscal adjustment (on spending and revenue) and freeing up the tariffs. However some measures to effect must be approved by the Senate by the end of May, once they expire on July 1. 3/ 5 Now 38

39 Sovereign Ratings Brazilian Sovereign Credit Ratings S&P downgraded, on March 2014, Brazil's long-term foreign currency sovereign rating one notch to BBB-, adopting a stable outlook. Moody s and Fitch agencies have indicated a likely downgrade in case of no improvements on fiscal accounts and inflation/growth performances. On March 2015, S&P maintained Brazil s long term sovereign rating in BBB-, keeping a stable outlook due to the economic policy changes proposed by the government. Outlook Positive Stable Negative Source: Rating Agencies, FCF 4/ 5 39

40 Sovereign Ratings Fiscal deterioration and Growing Debt Focus on Economic Team (% GDP) Monetary tightening Fiscal adjustment Fx adjustment (End of BCB swap program) Brazil economic challenges have increased Economic recession High inflation Fiscal deterioration and growing debt Low growth and High Inflation Downside risks Inflation Growth Market expectation * % yoy Low confidence indexes and low growth Challenging external conditions Corruption scandals and complex political system Sustainability of the adjustment process Lack of microeconomic reform agenda * Based on Focus research, April 10th, 2015 Source: Rating Agencies, Fitch 5/ 5 40

41 Politic 41

42 Dilma s Approval After Dilma Rousseff s reelection, the disclosure of several corruption scandals, depreciation of the local currency, the upward trend of inflation and the labor market deterioration, Datafolha reported strong decline in government approval, reaching now 62% of disapproval. In addition, the fiscal adjustments in place and cuts in social benefit entitlements are likely bring about a decline in political support from unions and social movements, which are among the most traditional supporters of the ruling PT. Source: TSE, FCF 1/ 2 42

43 Confidence Index The sharp fall presented since the beginning of the 2014 is still downhill. In 2015 the confidence index already reached the worst level since This result was motivated by the worsening of domestic scenario, the expectations and the worries about labor market, inflation and the risk of water and electricity shortage. 125 Confidence Index Social Movements 120 World Cup , ,1 Source: FGV, CNI, FCF Consumer Confidence Index Industry Confidence Index 2/ 2 43

ADJUSTMENTS IN BRAZIL S ECONOMIC POLICY IN 2015 WILL LIKELY PRODUCE MORE SUSTAINABLE GDP GROWTH RATES GOING FORWARD

PRESENTATION APIMEC BRASÍLIA ADJUSTMENTS IN BRAZIL S ECONOMIC POLICY IN 2015 WILL LIKELY PRODUCE MORE SUSTAINABLE GDP GROWTH RATES GOING FORWARD 1 1 Brasília, February, 5th 2015 Ellen Regina Steter WORLD

PRESENTATION APIMEC BRASÍLIA ADJUSTMENTS IN BRAZIL S ECONOMIC POLICY IN 2015 WILL LIKELY PRODUCE MORE SUSTAINABLE GDP GROWTH RATES GOING FORWARD 1 1 Brasília, February, 5th 2015 Ellen Regina Steter WORLD

WWW.ADINOEL.COM Adinoél Sebastião /// Inglês Tradução Livre 14/2014

TEXTO Brazil Leads Decline Among World's Biggest Companies THE losses OF São Paulo's stock market AND THE decline OF Brazil's real made Brazilian companies THE biggest losers among THE world's major companies,

TEXTO Brazil Leads Decline Among World's Biggest Companies THE losses OF São Paulo's stock market AND THE decline OF Brazil's real made Brazilian companies THE biggest losers among THE world's major companies,

1. THE ANGOLAN ECONOMY

BPC IN BRIEF ÍNDICE 1. THE ANGOLAN ECONOMY 2. EVOLUTION OF THE BANK SECTOR 3. SHAREHOLDERS 4. BPC MARKET RANKING 5. FINANCIAL INDICATORES 6. PROJECTS FINANCE 7. GERMAN CORRESPONDENTS 1. THE ANGOLAN ECONOMY

BPC IN BRIEF ÍNDICE 1. THE ANGOLAN ECONOMY 2. EVOLUTION OF THE BANK SECTOR 3. SHAREHOLDERS 4. BPC MARKET RANKING 5. FINANCIAL INDICATORES 6. PROJECTS FINANCE 7. GERMAN CORRESPONDENTS 1. THE ANGOLAN ECONOMY

Active Ageing: Problems and Policies in Portugal. Francisco Madelino Berlin, 17 October 2006

Active Ageing: Problems and Policies in Portugal Francisco Madelino Berlin, 17 October 2006 ACTIVE AGEING 1. Demographic Trends in Portugal 2. Financial Implications of the Active Ageing on Social Security

Active Ageing: Problems and Policies in Portugal Francisco Madelino Berlin, 17 October 2006 ACTIVE AGEING 1. Demographic Trends in Portugal 2. Financial Implications of the Active Ageing on Social Security

International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China. dossiers. Economic Outlook Conjuntura Económica

dossiers Economic Outlook Conjuntura Económica International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China Last Update Última Actualização: 10-02-2015 Prepared

dossiers Economic Outlook Conjuntura Económica International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China Last Update Última Actualização: 10-02-2015 Prepared

Qualquer similaridade é mera coincidência? a. Venda doméstica de automóveis na Coréia (y-o-y, %)

") Brasil e Coréia: Qualquer similaridade é mera coincidência? a Faz algum tempo que argumentamos sobre as lições importantes que a Coréia oferece ao Brasil. O país possui grau de investimento há muitos anos,

Brasil e Coréia: Qualquer similaridade é mera coincidência? a Faz algum tempo que argumentamos sobre as lições importantes que a Coréia oferece ao Brasil. O país possui grau de investimento há muitos anos,

106 BANCO DE PORTUGAL Boletim Estatístico

106 BANCO DE PORTUGAL Boletim Estatístico B.7.1.1 Taxas de juro sobre novas operações de empréstimos (1) concedidos por instituições financeiras monetárias a residentes na área do euro (a) Interest rates

106 BANCO DE PORTUGAL Boletim Estatístico B.7.1.1 Taxas de juro sobre novas operações de empréstimos (1) concedidos por instituições financeiras monetárias a residentes na área do euro (a) Interest rates

Adinoél Sebastião /// Inglês Tradução Livre 49/2013

TEXTO Brazilian Central Bank Increases Interest Rates Third Consecutive Time In another step to combat high inflation, yesterday the Brazilian Central Bank raised interest rates for the third time in a

TEXTO Brazilian Central Bank Increases Interest Rates Third Consecutive Time In another step to combat high inflation, yesterday the Brazilian Central Bank raised interest rates for the third time in a

Faturamento - 1966/2008 Revenue - 1966/2008

1.6 Faturamento 1966/008 Revenue 1966/008 1966 1967 1968 1969 1970 1971 197 1973 1974 1975 1976 1977 1978 1979 198 AUTOVEÍCULOS VEHICLES 7.991 8.11 9.971 11.796 13.031 15.9 17.793 0.78 3.947 6.851 6.64

1.6 Faturamento 1966/008 Revenue 1966/008 1966 1967 1968 1969 1970 1971 197 1973 1974 1975 1976 1977 1978 1979 198 AUTOVEÍCULOS VEHICLES 7.991 8.11 9.971 11.796 13.031 15.9 17.793 0.78 3.947 6.851 6.64

REAL ESTATE MARKET IN BRAZIL

REAL ESTATE MARKET IN BRAZIL JOÃO CRESTANA President of Secovi SP and CBIC National Commission of Construction Industry SIZE OF BRAZIL Population distribution by gender, according to age group BRAZIL 2010

REAL ESTATE MARKET IN BRAZIL JOÃO CRESTANA President of Secovi SP and CBIC National Commission of Construction Industry SIZE OF BRAZIL Population distribution by gender, according to age group BRAZIL 2010

Cenário Econômico como Direcionador de Estratégias de Investimento no Brasil

Cenário Econômico como Direcionador de Estratégias de Investimento no Brasil VII Congresso Anbima de Fundos de Investimentos Rodrigo R. Azevedo Maio 2013 2 Principal direcionador macro de estratégias de

Cenário Econômico como Direcionador de Estratégias de Investimento no Brasil VII Congresso Anbima de Fundos de Investimentos Rodrigo R. Azevedo Maio 2013 2 Principal direcionador macro de estratégias de

Cenário Econômico para 2014

Cenário Econômico para 2014 Silvia Matos 18 de Novembro de 2013 Novembro de 2013 Cenário Externo As incertezas com relação ao cenário externo em 2014 são muito elevadas Do ponto de vista de crescimento,

Cenário Econômico para 2014 Silvia Matos 18 de Novembro de 2013 Novembro de 2013 Cenário Externo As incertezas com relação ao cenário externo em 2014 são muito elevadas Do ponto de vista de crescimento,

INTRODUCTION 3 A. CURRENT NET VALUE OF THE PORTFOLIO (IN MILLION USD) 4 B. GEOGRAPHICAL COMPOSITION BY DURATION 4

4 B. GEOGRAPHICAL COMPOSITION BY DURATION 4") TABLE OF CONTENTS INTRODUCTION 3 A. CURRENT NET VALUE OF THE PORTFOLIO (IN MILLION USD) 4 B. GEOGRAPHICAL COMPOSITION BY DURATION 4 C. PORTFOLIO COMPOSITION BY ASSET CLASSES 5 D. HOLDINGS WITH HIGH AND

TABLE OF CONTENTS INTRODUCTION 3 A. CURRENT NET VALUE OF THE PORTFOLIO (IN MILLION USD) 4 B. GEOGRAPHICAL COMPOSITION BY DURATION 4 C. PORTFOLIO COMPOSITION BY ASSET CLASSES 5 D. HOLDINGS WITH HIGH AND

WWW.ADINOEL.COM Adinoél Sebastião /// Inglês Tradução Livre 67/2013

PASSO A PASSO DO DYNO Ao final desse passo a passo você terá o texto quase todo traduzido. Passo 1 Marque no texto as palavras abaixo. (decore essas palavras, pois elas aparecem com muita frequência nos

PASSO A PASSO DO DYNO Ao final desse passo a passo você terá o texto quase todo traduzido. Passo 1 Marque no texto as palavras abaixo. (decore essas palavras, pois elas aparecem com muita frequência nos

Fonte / Source: Banco Central Europeu / European Central Bank. Depósitos com pré-aviso até 3 meses. equiparados até 2 anos (1)

") B.0.1 AGREGADOS MONETÁRIOS DA ÁREA DO EURO (a) EURO AREA MONETARY AGGREGATES (a) Saldos em fim de mês End-of-month figures Fonte / Source: Banco Central Europeu / European Central Bank M3 Circulação monetária

B.0.1 AGREGADOS MONETÁRIOS DA ÁREA DO EURO (a) EURO AREA MONETARY AGGREGATES (a) Saldos em fim de mês End-of-month figures Fonte / Source: Banco Central Europeu / European Central Bank M3 Circulação monetária

International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China. dossiers. Economic Outlook Conjuntura Económica

dossiers Economic Outlook Conjuntura Económica International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China Last Update Última Actualização: 14-03-2016 Prepared

dossiers Economic Outlook Conjuntura Económica International Trade and FDI between Portugal-China Comércio Internacional e IDE entre Portugal-China Last Update Última Actualização: 14-03-2016 Prepared

Rating soberano do Brasil

Rating soberano do Brasil Regina Nunes Presidente Standard & Poor s no Brasil Outubro 2014 Permission to reprint or distribute any content from this presentation requires the prior written approval of

Rating soberano do Brasil Regina Nunes Presidente Standard & Poor s no Brasil Outubro 2014 Permission to reprint or distribute any content from this presentation requires the prior written approval of

Apresentação Semanal. De 18 a 29 de abril de Tatiana Pinheiro

1 Apresentação Semanal De 18 a 29 de abril de 2016 Tatiana Pinheiro tatiana.pinheiro@santander.com.br Indicadores e eventos da última semana Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12 Feb-13

1 Apresentação Semanal De 18 a 29 de abril de 2016 Tatiana Pinheiro tatiana.pinheiro@santander.com.br Indicadores e eventos da última semana Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12 Feb-13

Março / 2015. Cenário Econômico Bonança e Tempestade. Departamento de Pesquisas e Estudos Econômicos

Março / 2015 Cenário Econômico Bonança e Tempestade Departamento de Pesquisas e Estudos Econômicos 1 Bonança Externa Boom das Commodities Estímulos ao consumo X inflação Importações e real valorizado 2

Março / 2015 Cenário Econômico Bonança e Tempestade Departamento de Pesquisas e Estudos Econômicos 1 Bonança Externa Boom das Commodities Estímulos ao consumo X inflação Importações e real valorizado 2

Brazil and Latin America Economic Outlook

Brazil and Latin America Economic Outlook Minister Paulo Bernardo Washington, 13 de maio de 2009 Apresentação Impactos da Crise Econômica Situação Econômica Brasileira Ações Contra-Cíclicas Previsões para

Brazil and Latin America Economic Outlook Minister Paulo Bernardo Washington, 13 de maio de 2009 Apresentação Impactos da Crise Econômica Situação Econômica Brasileira Ações Contra-Cíclicas Previsões para

Growth of 11.2% in the Net Revenue. Parent R$ 2.2 bi % Consolidated R$ 4.0 bi % Growth of 1.1 p.p. in the Gross Margin

Results 3Q15 GMV Net Revenue SSS Growth GMV reached R$ 4.9 billion Growth of 11.2% in the Net Revenue Net Revenue in the same stores sales concept grew 9% in the quarter Parent R$ 2.2 bi. +11.2% Consolidated

Results 3Q15 GMV Net Revenue SSS Growth GMV reached R$ 4.9 billion Growth of 11.2% in the Net Revenue Net Revenue in the same stores sales concept grew 9% in the quarter Parent R$ 2.2 bi. +11.2% Consolidated

Consolidated Results for the 1st Quarter 2017

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

CENÁRIOS ECONÔMICOS O QUE ESPERAR DE 2016? Prof. Antonio Lanzana Dezembro/2015

CENÁRIOS ECONÔMICOS O QUE ESPERAR DE 2016? Prof. Antonio Lanzana Dezembro/2015 1 SUMÁRIO 1. Economia Mundial e Impactos sobre o Brasil 2. Política Econômica Desastrosa do Primeiro Mandato 2.1. Resultados

CENÁRIOS ECONÔMICOS O QUE ESPERAR DE 2016? Prof. Antonio Lanzana Dezembro/2015 1 SUMÁRIO 1. Economia Mundial e Impactos sobre o Brasil 2. Política Econômica Desastrosa do Primeiro Mandato 2.1. Resultados

Informacao Publica Inicial. Estado de Mato Grosso. 27 de agosto de 2012

Informacao Publica Inicial Estado de Mato Grosso 27 de agosto de 2012 Item 1 Item 2 Item 3 Exportacao Brasileira, ranking por Estados entre 2008 e 2011 Comercio Exterior Mato-Grossense Evolucao das Exportacoes

Informacao Publica Inicial Estado de Mato Grosso 27 de agosto de 2012 Item 1 Item 2 Item 3 Exportacao Brasileira, ranking por Estados entre 2008 e 2011 Comercio Exterior Mato-Grossense Evolucao das Exportacoes

Brasil: Crescimento Sustentável, Distribuição de Renda e Inclusão Social. Miami Ministro Paulo Bernardo 6 de Abril de 2008

Brasil: Crescimento Sustentável, Distribuição de Renda e Inclusão Social Miami Ministro Paulo Bernardo 6 de Abril de 2008 Brasil consolida um mercado de consumo de massa e promove o surgimento de uma nova

Brasil: Crescimento Sustentável, Distribuição de Renda e Inclusão Social Miami Ministro Paulo Bernardo 6 de Abril de 2008 Brasil consolida um mercado de consumo de massa e promove o surgimento de uma nova

Inserção internacional

Apostila Inserção Internacional 2017/18 Antony P. Mueller UFS Inserção internacional Livre comércio Investimentos estrangeiros Integração regional Dívida externa Exportação estratégica Etapas na criação

Apostila Inserção Internacional 2017/18 Antony P. Mueller UFS Inserção internacional Livre comércio Investimentos estrangeiros Integração regional Dívida externa Exportação estratégica Etapas na criação

Conference Call 2Q13 and 1H13 Results

Conference Call 2Q13 and 1H13 Results 2 Performance in the Negócios Internacionais Negócios domestic Nacionais and USA,Europa e international markets Exportações Márcio Utsch Net Revenue 3 Net revenue

Conference Call 2Q13 and 1H13 Results 2 Performance in the Negócios Internacionais Negócios domestic Nacionais and USA,Europa e international markets Exportações Márcio Utsch Net Revenue 3 Net revenue

Perspectivas 2014 Brasil e Mundo

1 Perspectivas 2014 Brasil e Mundo 2 Agenda EUA: Fim dos estímulos em 2013? China: Hard landing? Zona do Euro: Crescimento econômico? Brasil: Deixamos de ser rumo de investimentos? EUA Manutenção de estímulos

1 Perspectivas 2014 Brasil e Mundo 2 Agenda EUA: Fim dos estímulos em 2013? China: Hard landing? Zona do Euro: Crescimento econômico? Brasil: Deixamos de ser rumo de investimentos? EUA Manutenção de estímulos

Multicriteria Impact Assessment of the certified reference material for ethanol in water

Multicriteria Impact Assessment of the certified reference material for ethanol in water André Rauen Leonardo Ribeiro Rodnei Fagundes Dias Taiana Fortunato Araujo Taynah Lopes de Souza Inmetro / Brasil

Multicriteria Impact Assessment of the certified reference material for ethanol in water André Rauen Leonardo Ribeiro Rodnei Fagundes Dias Taiana Fortunato Araujo Taynah Lopes de Souza Inmetro / Brasil

SINOPSE DE CLIPPING SEMANAL SINDISIDER

SINOPSE DE CLIPPING SEMANAL SINDISIDER 1ª SEMANA DE MARÇO O Press Release divulgado pela SD&PRESS Consultoria, que aborda os números do setor de distribuição de aços planos em fevereiro, recebeu destaque

SINOPSE DE CLIPPING SEMANAL SINDISIDER 1ª SEMANA DE MARÇO O Press Release divulgado pela SD&PRESS Consultoria, que aborda os números do setor de distribuição de aços planos em fevereiro, recebeu destaque

COSEC. Valorização do Real e Mercado Futuro de Câmbio

COSEC 8 de Agosto de 2011 Valorização do Real e Mercado Futuro de Câmbio Roberto Giannetti da Fonseca Diretor Titular Departamento de Relações Internacionais e Comércio Exterior Mitos e Mistérios do Mercado

COSEC 8 de Agosto de 2011 Valorização do Real e Mercado Futuro de Câmbio Roberto Giannetti da Fonseca Diretor Titular Departamento de Relações Internacionais e Comércio Exterior Mitos e Mistérios do Mercado

ABDIB Associação Brasileira da Infra-estrutura e Indústrias de base

ABDIB Associação Brasileira da Infra-estrutura e Indústrias de base Cenário Econômico Internacional & Brasil Prof. Dr. Antonio Corrêa de Lacerda antonio.lacerda@siemens.com São Paulo, 14 de março de 2007

ABDIB Associação Brasileira da Infra-estrutura e Indústrias de base Cenário Econômico Internacional & Brasil Prof. Dr. Antonio Corrêa de Lacerda antonio.lacerda@siemens.com São Paulo, 14 de março de 2007

October, 2013. Um Olhar Estratégico para o Setor de Seguros de Automóvel no Brasil

October, 2013 Um Olhar Estratégico para o Setor de Seguros de Automóvel no Brasil AGENDA Visão da Industria de Seguros (Brasil x Mundo) Drivers que movem a Indústria Análise da Penetração da Indústria

October, 2013 Um Olhar Estratégico para o Setor de Seguros de Automóvel no Brasil AGENDA Visão da Industria de Seguros (Brasil x Mundo) Drivers que movem a Indústria Análise da Penetração da Indústria

Classificação da Informação: Uso Irrestrito

Cenário Econômico Qual caminho escolheremos? Cenário Econômico 2015 Estamos no caminho correto? Estamos no caminho correto? Qual é nossa visão sobre a economia? Estrutura da economia sinaliza baixa capacidade

Cenário Econômico Qual caminho escolheremos? Cenário Econômico 2015 Estamos no caminho correto? Estamos no caminho correto? Qual é nossa visão sobre a economia? Estrutura da economia sinaliza baixa capacidade

Os impactos da Crise nas Receitas das Três Esferas de Governo

Os impactos da Crise nas Receitas das Três Esferas de Governo XXIII Seminario Regional de Politica Fiscal CEPAL Santiago de Chile, 18 al 21 de enero de 2011 Luis Felipe Vital Nunes Pereira Secretaria do

Os impactos da Crise nas Receitas das Três Esferas de Governo XXIII Seminario Regional de Politica Fiscal CEPAL Santiago de Chile, 18 al 21 de enero de 2011 Luis Felipe Vital Nunes Pereira Secretaria do

Competitiveness in the Brazilian economy: challenges & opportunities

Competitiveness in the Brazilian economy: challenges & opportunities Erik Camarano MBC CEO Thursday, June 6th, 2013 Woodrow Wilson International Center for Scholars 6th Floor Auditorium SPONSORS SHORT-TERM

Competitiveness in the Brazilian economy: challenges & opportunities Erik Camarano MBC CEO Thursday, June 6th, 2013 Woodrow Wilson International Center for Scholars 6th Floor Auditorium SPONSORS SHORT-TERM

Processo de exportação de perecíveis aos EUA. (Frederico Tavares - Gerente de Comércio Internacional, UGBP: Union of Growers of Brazilian Papaya)

") Processo de exportação de perecíveis aos EUA (Frederico Tavares - Gerente de Comércio Internacional, UGBP: Union of Growers of Brazilian Papaya) World Production of Tropical Fruit World production of tropical

Processo de exportação de perecíveis aos EUA (Frederico Tavares - Gerente de Comércio Internacional, UGBP: Union of Growers of Brazilian Papaya) World Production of Tropical Fruit World production of tropical

ECONOMIA BRASILEIRA DESEMPENHO RECENTE E CENÁRIOS PARA 2015. Prof. Antonio Lanzana Dezembro/2014

ECONOMIA BRASILEIRA DESEMPENHO RECENTE E CENÁRIOS PARA 2015 Prof. Antonio Lanzana Dezembro/2014 SUMÁRIO 1. Economia Mundial e Impactos sobre o Brasil 2. A Economia Brasileira Atual 2.1. Desempenho Recente

ECONOMIA BRASILEIRA DESEMPENHO RECENTE E CENÁRIOS PARA 2015 Prof. Antonio Lanzana Dezembro/2014 SUMÁRIO 1. Economia Mundial e Impactos sobre o Brasil 2. A Economia Brasileira Atual 2.1. Desempenho Recente

MACROECONOMIC OUTLOOK

MACROECONOMIC OUTLOOK DETERMINED BY CHANGES IN THE GLOBAL OUTLOOK AND ITS IMPACTS ON EXCHANGE-RATE AND BY THE SLOWER DOMESTIC GROWTH Economic Research Department - DEPEC 1984 1985 1986 1987 1988 1989 1990

MACROECONOMIC OUTLOOK DETERMINED BY CHANGES IN THE GLOBAL OUTLOOK AND ITS IMPACTS ON EXCHANGE-RATE AND BY THE SLOWER DOMESTIC GROWTH Economic Research Department - DEPEC 1984 1985 1986 1987 1988 1989 1990

PORTUGAL Indicadores de Conjuntura Economic Short term Indicators

Produção e Volume de Negócios / Production and Turnover Índice de Produção Industrial Industrial Production Index vh y o y 1,5 1,9 4,4 5,7 6,3 3,8 0,1 2,1 9,2 x 4,2 4,4 5,0 x Indústria Transformadora vh

Produção e Volume de Negócios / Production and Turnover Índice de Produção Industrial Industrial Production Index vh y o y 1,5 1,9 4,4 5,7 6,3 3,8 0,1 2,1 9,2 x 4,2 4,4 5,0 x Indústria Transformadora vh

Salário mínimo tem reajuste de apenas 1,81% 11/01/2018

e GRUPO DE ESTUDO DE POLÍTICAS MACROECONÔMICAS E CRESCIMENTO ECONÔMICO DEPARTAMENTO DE CIÊNCIAS ECONÔMICAS (DCECO) - UNIVERSIDADE FEDERAL DE SÃO JOÃO DEL REI - UFSJ RADAR DA ECONOMIA (semanal) 2ª edição/2018

e GRUPO DE ESTUDO DE POLÍTICAS MACROECONÔMICAS E CRESCIMENTO ECONÔMICO DEPARTAMENTO DE CIÊNCIAS ECONÔMICAS (DCECO) - UNIVERSIDADE FEDERAL DE SÃO JOÃO DEL REI - UFSJ RADAR DA ECONOMIA (semanal) 2ª edição/2018

SECTOR OF ACTIVIITY FOOD ENERGY COTTON BIODIESEL SOYA VEGETAL OIL CORN ETHANOL

Results 08/15/2011 SECTOR OF ACTIVIITY FOOD ENERGY COTTON SOYA CORN BIODIESEL VEGETAL OIL ETHANOL BRAZILIAN BIODIESEL MARKET 2005 2007 Blend: up to 2% 1st Sem/08 Blend: min. 2% Jul/08 Jun/09 Blend: min.

Results 08/15/2011 SECTOR OF ACTIVIITY FOOD ENERGY COTTON SOYA CORN BIODIESEL VEGETAL OIL ETHANOL BRAZILIAN BIODIESEL MARKET 2005 2007 Blend: up to 2% 1st Sem/08 Blend: min. 2% Jul/08 Jun/09 Blend: min.

Sistema Financeiro e os Fundamentos para o Crescimento

Sistema Financeiro e os Fundamentos para o Crescimento Henrique de Campos Meirelles Novembro de 20 1 Fundamentos macroeconômicos sólidos e medidas anti-crise 2 % a.a. Inflação na meta 8 6 metas cumpridas

Sistema Financeiro e os Fundamentos para o Crescimento Henrique de Campos Meirelles Novembro de 20 1 Fundamentos macroeconômicos sólidos e medidas anti-crise 2 % a.a. Inflação na meta 8 6 metas cumpridas

Cenário Econômico Brasil em uma nova ordem mundial. Guilherme Mercês Sistema FIRJAN

Cenário Econômico Brasil em uma nova ordem mundial Guilherme Mercês Sistema FIRJAN Cenário Internacional Cenário mundial ainda cercado de incertezas (1) EUA: Recuperação lenta; juros à frente (2) Europa:

Cenário Econômico Brasil em uma nova ordem mundial Guilherme Mercês Sistema FIRJAN Cenário Internacional Cenário mundial ainda cercado de incertezas (1) EUA: Recuperação lenta; juros à frente (2) Europa:

Economic Research - Brasil Apresentação Semanal. De 02 a 06 de Abril de Mirella Pricoli Amaro Hirakawa

Economic Research - Brasil 2018 Apresentação Semanal De 02 a 06 de Abril de 2018 Mirella Pricoli Amaro Hirakawa mhirakawa@santander.com.br Relatórios Relatório de Crédito 3 3 Relatório Câmbio 4 4 Relatório

Economic Research - Brasil 2018 Apresentação Semanal De 02 a 06 de Abril de 2018 Mirella Pricoli Amaro Hirakawa mhirakawa@santander.com.br Relatórios Relatório de Crédito 3 3 Relatório Câmbio 4 4 Relatório

PERSPECTIVAS MACROECONÔMICAS E OS IMPACTOS NAS ALOCAÇÕES DAS EFPCs

PERSPECTIVAS MACROECONÔMICAS E OS IMPACTOS NAS ALOCAÇÕES DAS EFPCs Brazil: Large growth underperformance, but not FX underperformance 13Q1 13Q1 13Q1 13Q1 14Q1 14Q1 14Q1 14Q1 15Q1 15Q1 15Q1 15Q1 16Q1 16Q1

PERSPECTIVAS MACROECONÔMICAS E OS IMPACTOS NAS ALOCAÇÕES DAS EFPCs Brazil: Large growth underperformance, but not FX underperformance 13Q1 13Q1 13Q1 13Q1 14Q1 14Q1 14Q1 14Q1 15Q1 15Q1 15Q1 15Q1 16Q1 16Q1

VII Encontro Empresarial Ibero-Americano

VII Encontro Empresarial Ibero-Americano A gestão dos riscos: Os preços das matérias primas, a inflação e os movimentos de capital FIT FOR A NEW ERA 27 de Outubro de 2011 Estrutura da apresentação 1 Uma

VII Encontro Empresarial Ibero-Americano A gestão dos riscos: Os preços das matérias primas, a inflação e os movimentos de capital FIT FOR A NEW ERA 27 de Outubro de 2011 Estrutura da apresentação 1 Uma

MB ASSOCIADOS CENÁRIO MACROECONÔMICO BRASILEIRO. Sergio Vale Economista-chefe

MB ASSOCIADOS CENÁRIO MACROECONÔMICO BRASILEIRO Sergio Vale Economista-chefe I. Economia Internacional II. Economia Brasileira Comparação entre a Grande Depressão de 30 e a Grande Recessão de 08/09 Produção

MB ASSOCIADOS CENÁRIO MACROECONÔMICO BRASILEIRO Sergio Vale Economista-chefe I. Economia Internacional II. Economia Brasileira Comparação entre a Grande Depressão de 30 e a Grande Recessão de 08/09 Produção

Trends and Business Opportunities in Latin America

Trends and Business Opportunities in Latin America Hamilton Terni Costa ANconsulting ANconsulting LA overview Latin America is composed of South and Central America, Mexico and Caribbean 20 countries in

Trends and Business Opportunities in Latin America Hamilton Terni Costa ANconsulting ANconsulting LA overview Latin America is composed of South and Central America, Mexico and Caribbean 20 countries in

Parte 1 Part 1. Mercado das Comunicações. na Economia Nacional (2006-2010)

") Parte 1 Part 1 Mercado das Comunicações na Economia Nacional (2006-2010) Communications Market in National Economy (2006/2010) Parte 1 Mercado das Comunicações na Economia Nacional (2006-2010) / Part 1

Parte 1 Part 1 Mercado das Comunicações na Economia Nacional (2006-2010) Communications Market in National Economy (2006/2010) Parte 1 Mercado das Comunicações na Economia Nacional (2006-2010) / Part 1

Observações sobre o Reequilíbrio Fiscal no Brasil

Observações sobre o Reequilíbrio Fiscal no Brasil Nelson Barbosa Ministério do Planejamento, Orçamento e Gestão 1º de junho de 2015 Cenário Macroeconômico e Reequilíbrio Fiscal O governo está elevando

Observações sobre o Reequilíbrio Fiscal no Brasil Nelson Barbosa Ministério do Planejamento, Orçamento e Gestão 1º de junho de 2015 Cenário Macroeconômico e Reequilíbrio Fiscal O governo está elevando

Definição de competitividade

TRIBUTAÇÃO E COMPETITIVIDADE VII Jornadas do IPCA 25.11.2006 Claudia Dias Soares Universidade Católica Portuguesa Definição de competitividade EC 2004: a sustained rise in the standards of living of a

TRIBUTAÇÃO E COMPETITIVIDADE VII Jornadas do IPCA 25.11.2006 Claudia Dias Soares Universidade Católica Portuguesa Definição de competitividade EC 2004: a sustained rise in the standards of living of a

1- Cenário Macroeconômico

RELATÓRIO PREVI NOVARTIS 1 de Abril de 214 1- Cenário Macroeconômico No cenário global, o evento chave foi a reunião de política monetária do banco central americano, o FED, que sinalizou a continuidade

RELATÓRIO PREVI NOVARTIS 1 de Abril de 214 1- Cenário Macroeconômico No cenário global, o evento chave foi a reunião de política monetária do banco central americano, o FED, que sinalizou a continuidade

RADAR DA ECONOMIA (semanal) Provocação 08/2016 Grupo de Estudo de Políticas Macroeconômicas e Crescimento Econômico São João del Rei, 14/04/2016.

Provocação 08/2016 Grupo de Estudo de Políticas Macroeconômicas e Crescimento Econômico São João del Rei, 14/04/2016.") GRUPO DE ESTUDO DE POLÍTICAS MACROECONÔMICAS E CRESCIMENTO ECONÔMICO DEPARTAMENTO DE CIÊNCIAS ECONÔMICAS (DCECO) - UNIVERSIDADE FEDERAL DE SÃO JOÃO DEL REI - UFSJ RADAR DA ECONOMIA (semanal) Provocação

GRUPO DE ESTUDO DE POLÍTICAS MACROECONÔMICAS E CRESCIMENTO ECONÔMICO DEPARTAMENTO DE CIÊNCIAS ECONÔMICAS (DCECO) - UNIVERSIDADE FEDERAL DE SÃO JOÃO DEL REI - UFSJ RADAR DA ECONOMIA (semanal) Provocação

X SEMINÁRIO SUL BRASILEIRO DE PREVIDÊNCIA PÚBLICA. BENTO GONÇALVES / RS / Maio 2012

X SEMINÁRIO SUL BRASILEIRO DE PREVIDÊNCIA PÚBLICA BENTO GONÇALVES / RS / Maio 2012 CENÁRIO INTERNACIONAL ESTADOS UNIDOS Ø Abrandamento da política monetária para promover o crescimento sustentável. Ø Sinais

X SEMINÁRIO SUL BRASILEIRO DE PREVIDÊNCIA PÚBLICA BENTO GONÇALVES / RS / Maio 2012 CENÁRIO INTERNACIONAL ESTADOS UNIDOS Ø Abrandamento da política monetária para promover o crescimento sustentável. Ø Sinais

Adinoél Sebastião /// Inglês Tradução Livre 20/2013

TEXTO WWW.ADINOEL.COM Spending for the 2014 World Cup in Brazil explodes beyond prediction and reaches R$ 26.5 billion The cost for organizing the 2014 World Cup has now reached R$26.5 billion. The figure

TEXTO WWW.ADINOEL.COM Spending for the 2014 World Cup in Brazil explodes beyond prediction and reaches R$ 26.5 billion The cost for organizing the 2014 World Cup has now reached R$26.5 billion. The figure

Consolidated Results 4th Quarter 2016

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

Consolidated Results for the 1st Quarter 2016

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

SAG GEST Soluções Automóvel Globais, SGPS, SA Listed Company Estrada de Alfragide, nº 67, Amadora Registered Share Capital: 169,764,398 euros Registered at the Amadora Registrar of Companies under the

Consultoria. Crise econômica - o que ainda está por vir e os impactos na hotelaria. Novembro/2015. Juan Jensen jensen@4econsultoria.com.

Consultoria Crise econômica - o que ainda está por vir e os impactos na hotelaria Novembro/2015 Juan Jensen jensen@4econsultoria.com.br Cenário Político DilmaI: governo ruim, centralizador e diagnóstico

Consultoria Crise econômica - o que ainda está por vir e os impactos na hotelaria Novembro/2015 Juan Jensen jensen@4econsultoria.com.br Cenário Político DilmaI: governo ruim, centralizador e diagnóstico

Fórum Permanente de Micro e Pequenas Empresas. Comitê de Comércio Exterior. Brasília Julho de 2011

Fórum Permanente de Micro e Pequenas Empresas Comitê de Comércio Exterior Brasília Julho de 2011 BALANÇA BRASILEIRA DE COMÉRCIO EXTERIOR DE BENS E SERVIÇOS* US$ Bilhões BRAZILIAN FOREIGN TRADE IN GOODS

Fórum Permanente de Micro e Pequenas Empresas Comitê de Comércio Exterior Brasília Julho de 2011 BALANÇA BRASILEIRA DE COMÉRCIO EXTERIOR DE BENS E SERVIÇOS* US$ Bilhões BRAZILIAN FOREIGN TRADE IN GOODS

Quem Paga a Conta? Rodrigo R. Azevedo. Setembro 2013

Quem Paga a Conta? Rodrigo R. Azevedo Setembro 2013 2 Melhoras institucionais do Brasil desde 1994: aceleração do crescimento e queda da inflação 9% Brasil: Crescimento do PIB 24% IPCA Inflação Anual 7%

Quem Paga a Conta? Rodrigo R. Azevedo Setembro 2013 2 Melhoras institucionais do Brasil desde 1994: aceleração do crescimento e queda da inflação 9% Brasil: Crescimento do PIB 24% IPCA Inflação Anual 7%

Juros caem em semana de forte ingresso de capital estrangeiro no mercado;

31-mar-2014 Juros caem em semana de forte ingresso de capital estrangeiro no mercado; Dólar se deprecia 2,7% na semana, influenciado por entrada de fluxo positivo; Ibovespa sobe 5,0% na semana, se aproximando

31-mar-2014 Juros caem em semana de forte ingresso de capital estrangeiro no mercado; Dólar se deprecia 2,7% na semana, influenciado por entrada de fluxo positivo; Ibovespa sobe 5,0% na semana, se aproximando

Interim Report Third Quarter 2003 November 3, 2003

Interim Report Third Quarter 2003 November 3, 2003 Q3 at a glance Structural changes vs 2002 -Tampere business consolidated from Q1 2003 -Eniro 118 118 consolidated from May 1, 2003 -Closure of Windhager

Interim Report Third Quarter 2003 November 3, 2003 Q3 at a glance Structural changes vs 2002 -Tampere business consolidated from Q1 2003 -Eniro 118 118 consolidated from May 1, 2003 -Closure of Windhager

Project Management Activities

Id Name Duração Início Término Predecessoras 1 Project Management Activities 36 dias Sex 05/10/12 Sex 23/11/12 2 Plan the Project 36 dias Sex 05/10/12 Sex 23/11/12 3 Define the work 15 dias Sex 05/10/12

Id Name Duração Início Término Predecessoras 1 Project Management Activities 36 dias Sex 05/10/12 Sex 23/11/12 2 Plan the Project 36 dias Sex 05/10/12 Sex 23/11/12 3 Define the work 15 dias Sex 05/10/12

Apresentação Semanal. De 19 a 23 de Dezembro de Everton Gomes

1 Apresentação Semanal De 19 a 23 de Dezembro de 2016 Everton Gomes everton.gomes@santander.com.br Visite o nosso site! www.santander.com.br/economia 2 2 Indicadores e eventos da última semana Internacional:

1 Apresentação Semanal De 19 a 23 de Dezembro de 2016 Everton Gomes everton.gomes@santander.com.br Visite o nosso site! www.santander.com.br/economia 2 2 Indicadores e eventos da última semana Internacional:

January/2013. FipeZap House Asking Price Index

January/2013 FipeZap House Asking Price Index METHODOLOGY 2 Introduction Housing is the most relevant item in household budget (32% in Brasil, according to POF/IBGE) Information on real estate prices is

January/2013 FipeZap House Asking Price Index METHODOLOGY 2 Introduction Housing is the most relevant item in household budget (32% in Brasil, according to POF/IBGE) Information on real estate prices is

Ministério da Fazenda. Crise Financeira. Impactos sobre o Brasil e Resposta do Governo. Nelson Barbosa. Novembro de 2008

1 Crise Financeira Impactos sobre o Brasil e Resposta do Governo Nelson Barbosa Novembro de 20 1 2 Impactos da Crise Financeira nas Economias Avançadas Primeiro impacto: grandes perdas patrimoniais, crise

1 Crise Financeira Impactos sobre o Brasil e Resposta do Governo Nelson Barbosa Novembro de 20 1 2 Impactos da Crise Financeira nas Economias Avançadas Primeiro impacto: grandes perdas patrimoniais, crise

Um Modelo Agregado de Consistência Macroeconômica para o Brasil

FUNDAÇÃO GETÚLIO VARGAS ESCOLA DE PÓS-GRADUAÇÃO EM ECONOMIA DISSERTAÇÃO DE MESTRADO Um Modelo Agregado de Consistência Macroeconômica para o Brasil Dissertação submetida à Escola de Pós-Graduação em Economia

FUNDAÇÃO GETÚLIO VARGAS ESCOLA DE PÓS-GRADUAÇÃO EM ECONOMIA DISSERTAÇÃO DE MESTRADO Um Modelo Agregado de Consistência Macroeconômica para o Brasil Dissertação submetida à Escola de Pós-Graduação em Economia

Overview. Resumo. dossiers. State and Government. Estado e Governo. Estado e Governo. State and Government Overview / Estado e Governo Resumo

dossiers State and Government Estado e State and Government Overview / Estado e Resumo State and Government Overview Estado e Resumo Last Update Última Actualização: 27/08/2015 Portugal Economy Probe (PE

dossiers State and Government Estado e State and Government Overview / Estado e Resumo State and Government Overview Estado e Resumo Last Update Última Actualização: 27/08/2015 Portugal Economy Probe (PE

Statistics Estatísticas do Mercado de Trabalho. Labour Market Statistics Estatísticas do Mercado de Trabalho. dossiers

dossiers Economic Outlook Conjuntura Last Update Última Atualização: 13-02-2015 Prepared by PE Probe Preparado por PE Probe Copyright 2015 Portugal Economy Probe PE Probe All rights reserved Index / Índice

dossiers Economic Outlook Conjuntura Last Update Última Atualização: 13-02-2015 Prepared by PE Probe Preparado por PE Probe Copyright 2015 Portugal Economy Probe PE Probe All rights reserved Index / Índice

05. Demonstrações Financeiras Financial Statements

05. Demonstrações Financeiras Financial Statements Demonstrações Financeiras Financial Statements 060 Balanços em 31 de Dezembro de 2007 e 2006 Balance at 31 December 2007 and 2006 Activo Assets 2007 2006

05. Demonstrações Financeiras Financial Statements Demonstrações Financeiras Financial Statements 060 Balanços em 31 de Dezembro de 2007 e 2006 Balance at 31 December 2007 and 2006 Activo Assets 2007 2006

Ajuste Macroeconômico na Economia Brasileira

Ajuste Macroeconômico na Economia Brasileira Fundação Getúlio Vargas 11º Fórum de Economia Ministro Guido Mantega Brasília, 15 de setembro de 2014 1 Por que fazer ajustes macroeconômicos? 1. Desequilíbrios

Ajuste Macroeconômico na Economia Brasileira Fundação Getúlio Vargas 11º Fórum de Economia Ministro Guido Mantega Brasília, 15 de setembro de 2014 1 Por que fazer ajustes macroeconômicos? 1. Desequilíbrios

MACROECONOMIC OUTLOOK: CHANGES IN THE GLOBAL OUTLOOK, DEEPER EXCHANGE-RATE DEPRECIATION AND SLOWER DOMESTIC GROWTH PROMPT ADJUSTMENTS IN OUR SCENARIO

MACROECONOMIC OUTLOOK: CHANGES IN THE GLOBAL OUTLOOK, DEEPER EXCHANGE-RATE DEPRECIATION AND SLOWER DOMESTIC GROWTH PROMPT ADJUSTMENTS IN OUR SCENARIO Economic Research Department - DEPEC 1980 1981 1982

MACROECONOMIC OUTLOOK: CHANGES IN THE GLOBAL OUTLOOK, DEEPER EXCHANGE-RATE DEPRECIATION AND SLOWER DOMESTIC GROWTH PROMPT ADJUSTMENTS IN OUR SCENARIO Economic Research Department - DEPEC 1980 1981 1982

Which model for agriculture? Dual model of Brazilian agriculture

Which model for agriculture? Dual model of Brazilian agriculture Sìlvia Helena Galvão de Miranda Professor Department of Economics, Business and Sociology ESALQ/USP Vice-coordinator CEPEA Pre-Conference

Which model for agriculture? Dual model of Brazilian agriculture Sìlvia Helena Galvão de Miranda Professor Department of Economics, Business and Sociology ESALQ/USP Vice-coordinator CEPEA Pre-Conference

Brazil: the good, the bad and the ugly. Economic Department

Brazil: the good, the bad and the ugly. Economic Department Scenario - International The Monetary War The Monetary War Total Assets of the Central Banks (US$ mi) $5.000 $4.500 $4.000 $3.500 $3.000 $2.500

Brazil: the good, the bad and the ugly. Economic Department Scenario - International The Monetary War The Monetary War Total Assets of the Central Banks (US$ mi) $5.000 $4.500 $4.000 $3.500 $3.000 $2.500

Perspectivas da Economia Brasileira

Perspectivas da Economia Brasileira CÂMARA DOS DEPUTADOS Ministro Guido Mantega Comissão de Fiscalização Financeira e Controle Comissão de Finanças e Tributação Brasília, 14 de maio de 2014 1 Economia

Perspectivas da Economia Brasileira CÂMARA DOS DEPUTADOS Ministro Guido Mantega Comissão de Fiscalização Financeira e Controle Comissão de Finanças e Tributação Brasília, 14 de maio de 2014 1 Economia

Notes on Cyclical tendency to the overvaluation of the real

Notes on Cyclical tendency to the overvaluation of the real Andre de Melo Modenesi (UFRJ and CNPq) Rui Lyrio Modenesi (Ex UFF) Paulo Gala (FGV SP) Objective This note addresses the question: To what extent

Notes on Cyclical tendency to the overvaluation of the real Andre de Melo Modenesi (UFRJ and CNPq) Rui Lyrio Modenesi (Ex UFF) Paulo Gala (FGV SP) Objective This note addresses the question: To what extent

Encontro de Bancos Centrais de países de língua portuguesa

Encontro de Bancos Centrais de países de língua portuguesa Antônio Gustavo Matos do Vale Diretor de Liquidações e Desestatização 4 de outubro de 2010 1 Evolução recente da economia brasileira O momento

Encontro de Bancos Centrais de países de língua portuguesa Antônio Gustavo Matos do Vale Diretor de Liquidações e Desestatização 4 de outubro de 2010 1 Evolução recente da economia brasileira O momento

Economic Research São Paulo - SP - Brasil Apresentação Semanal. De 20 a 24 de Agosto de Lucas Augusto (11)

") Economic Research São Paulo - SP - Brasil 2018 Apresentação Semanal De 20 a 24 de Agosto de 2018 Lucas Augusto (11) 3553-5263 Milhões Desafio dos Emergentes Dados do final de 2017, exceto taxas básicas

Economic Research São Paulo - SP - Brasil 2018 Apresentação Semanal De 20 a 24 de Agosto de 2018 Lucas Augusto (11) 3553-5263 Milhões Desafio dos Emergentes Dados do final de 2017, exceto taxas básicas

Subsidies and Tax Expenditures in Brazil Cepal Mansueto Almeida Secretary of Brazilian National Treasury

Subsidies and Tax Expenditures in Brazil Cepal Mansueto Almeida Secretary of Brazilian National Treasury March 26, 2019 2 Summary 11. General Overview 22. Tax Expenditures 31. Subsidies BNDES and Student

Subsidies and Tax Expenditures in Brazil Cepal Mansueto Almeida Secretary of Brazilian National Treasury March 26, 2019 2 Summary 11. General Overview 22. Tax Expenditures 31. Subsidies BNDES and Student

BRAZIL Economics Research

January 12 to 16 After the 2014 year-end holidays and a relatively calm start to 2015, market participants are slowly finding their bearings and getting acquainted with news flows again. Abroad, activity

January 12 to 16 After the 2014 year-end holidays and a relatively calm start to 2015, market participants are slowly finding their bearings and getting acquainted with news flows again. Abroad, activity

Economic Research São Paulo - SP - Brasil Apresentação Semanal. De 30 de Julho a 03 de Agosto de Rodolfo Margato (11)

") Economic Research São Paulo - SP - Brasil 2018 Apresentação Semanal De 30 de Julho a 03 de Agosto de 2018 Rodolfo Margato (11) 3553-1859 Estudo Inadimplência: Bem Melhor do que Parece 2 Estudo Inadimplência:

Economic Research São Paulo - SP - Brasil 2018 Apresentação Semanal De 30 de Julho a 03 de Agosto de 2018 Rodolfo Margato (11) 3553-1859 Estudo Inadimplência: Bem Melhor do que Parece 2 Estudo Inadimplência:

Principais indicadores económicos de Portugal Portugal - Main Economic Indicators

- Unidade/Unit DEMOGRAFIA - POPULAÇÃO E EMPRESAS DEMOGRAPHY - POPULATION AND CORPORATE População [1] Population [1] População Jovem (< 15 anos) [1] Youth Population [1] População Entre 15 e 64 anos [1]

- Unidade/Unit DEMOGRAFIA - POPULAÇÃO E EMPRESAS DEMOGRAPHY - POPULATION AND CORPORATE População [1] Population [1] População Jovem (< 15 anos) [1] Youth Population [1] População Entre 15 e 64 anos [1]

05. Demonstrações Financeiras Financial Statements

05. Demonstrações Financeiras Financial Statements Demonstrações Financeiras Financial Statements 068 Balanços em 31 de Dezembro de 2008 e 2007 Balance at 31 December 2008 and 2007 Activo Assets 2008 2007

05. Demonstrações Financeiras Financial Statements Demonstrações Financeiras Financial Statements 068 Balanços em 31 de Dezembro de 2008 e 2007 Balance at 31 December 2008 and 2007 Activo Assets 2008 2007

C.0.1 Balança de pagamentos Balance of payments

167 C.0.1 Balança de pagamentos Balance of payments Séries no Quadro/ Coluna 2016 2017 2018 Jan/18 Jan/19 Series in Table/ Column 2016 2017 2018 Jan/18 Jan/19 1 2 3 4 5 6 1 Balanças corrente e de capital...

167 C.0.1 Balança de pagamentos Balance of payments Séries no Quadro/ Coluna 2016 2017 2018 Jan/18 Jan/19 Series in Table/ Column 2016 2017 2018 Jan/18 Jan/19 1 2 3 4 5 6 1 Balanças corrente e de capital...

Resultado 1T18. Audioconferência 27 de Abril de :30 horas (horário de Brasília)

") Resultado 1T18 Audioconferência 27 de Abril de 2018 10:30 horas (horário de Brasília) Aviso Essa apresentação contém declarações que podem representar expectativas sobre eventos ou resultados futuros.

Resultado 1T18 Audioconferência 27 de Abril de 2018 10:30 horas (horário de Brasília) Aviso Essa apresentação contém declarações que podem representar expectativas sobre eventos ou resultados futuros.

Session 8 The Economy of Information and Information Strategy for e-business

Session 8 The Economy of Information and Information Strategy for e-business Information economics Internet strategic positioning Price discrimination Versioning Price matching The future of B2C InformationManagement

Session 8 The Economy of Information and Information Strategy for e-business Information economics Internet strategic positioning Price discrimination Versioning Price matching The future of B2C InformationManagement

FCL Capital March 2019

Performance FCL Hedge First Quarter 2019 6,48% First Quarter 2019 % CDI 428,76% Since Inception 13,16% Annualized since inception 5,86% FCL Opportunities First quarter 2019 in BRL 24,63% First quarter

Performance FCL Hedge First Quarter 2019 6,48% First Quarter 2019 % CDI 428,76% Since Inception 13,16% Annualized since inception 5,86% FCL Opportunities First quarter 2019 in BRL 24,63% First quarter

Workshop 2 Changes in Automotive Industry: New Markets Different Technologies?

Organization: Cooperation: Workshop 2 Changes in Automotive Industry: New Markets Different Technologies? Volkswagen do Brasil Cologne, August 25 th, 2008 Volkswagen do Brasil Present in Brazil since 1953

Organization: Cooperation: Workshop 2 Changes in Automotive Industry: New Markets Different Technologies? Volkswagen do Brasil Cologne, August 25 th, 2008 Volkswagen do Brasil Present in Brazil since 1953

As variáveis macroeconómicas importantes numa economia aberta incluem:

Aula Teórica nº 12 Sumário: Um modelo macroeconómico de economia aberta As variáveis macroeconómicas importantes numa economia aberta incluem: exportações líquidas investimento externo líquido taxas de

Aula Teórica nº 12 Sumário: Um modelo macroeconómico de economia aberta As variáveis macroeconómicas importantes numa economia aberta incluem: exportações líquidas investimento externo líquido taxas de

BUSINESS TO WORLD COMPANHIA GLOBAL DO VAREJO

BUSINESS TO WORLD COMPANHIA GLOBAL DO VAREJO 4Q08 Results Conference Call Friday: March 13, 2008 Time: 12:00 p.m (Brazil) 11:00 a.m (US EDT) Phone: +1 (888) 700.0802 (USA) +1 (786) 924.6977 (other countries)

BUSINESS TO WORLD COMPANHIA GLOBAL DO VAREJO 4Q08 Results Conference Call Friday: March 13, 2008 Time: 12:00 p.m (Brazil) 11:00 a.m (US EDT) Phone: +1 (888) 700.0802 (USA) +1 (786) 924.6977 (other countries)

WWW.ADINOEL.COM. Adinoél Sebastião /// Inglês Tradução Livre 61/2013. TEXTO In Ten Years of Bolsa Família, Federal Expenses with Assistance Triple

TEXTO In Ten Years of Bolsa Família, Federal Expenses with Assistance Triple In the ten years of the Bolsa Familia program, completed on Sunday, the biggest change in the federal government's budget was

TEXTO In Ten Years of Bolsa Família, Federal Expenses with Assistance Triple In the ten years of the Bolsa Familia program, completed on Sunday, the biggest change in the federal government's budget was

QUARTERLY MARKET REPORT

QUARTERLYMARKETREPORT SECONDQUARTER217 VOGELCONSULTING,LICENSEDINVESTMENTADVISORS,415GATEWAYROAD,BROOKFIELD,WI5455111 ECONOMICGROWTHDROVEEQUITYPRICESHIGHERBUTLEDTOHINTSOFCHANGESINCENTRALBANKPOLICIES FINANCIALMARKETS

QUARTERLYMARKETREPORT SECONDQUARTER217 VOGELCONSULTING,LICENSEDINVESTMENTADVISORS,415GATEWAYROAD,BROOKFIELD,WI5455111 ECONOMICGROWTHDROVEEQUITYPRICESHIGHERBUTLEDTOHINTSOFCHANGESINCENTRALBANKPOLICIES FINANCIALMARKETS

A Economia Brasileira e o Governo Dilma: Desafios e Oportunidades. Britcham São Paulo. Rubens Sardenberg Economista-chefe. 25 de fevereiro de 2011

A Economia Brasileira e o Governo Dilma: Desafios e Oportunidades Britcham São Paulo 25 de fevereiro de 2011 Rubens Sardenberg Economista-chefe Onde estamos? Indicadores de Conjuntura Inflação em alta

A Economia Brasileira e o Governo Dilma: Desafios e Oportunidades Britcham São Paulo 25 de fevereiro de 2011 Rubens Sardenberg Economista-chefe Onde estamos? Indicadores de Conjuntura Inflação em alta

Clique para editar o estilo do subtítulo mestre

Clique para editar o estilo do subtítulo mestre PMI Emergentes vs. PMI Desenvolvidos Global JP Morgan: PMI composto, manufatura e serviços sa ESTADOS UNIDOS EUA: PMI composto, manufatura e serviços sa

Clique para editar o estilo do subtítulo mestre PMI Emergentes vs. PMI Desenvolvidos Global JP Morgan: PMI composto, manufatura e serviços sa ESTADOS UNIDOS EUA: PMI composto, manufatura e serviços sa

O Brasil e a Crise Internacional

O Brasil e a Crise Internacional Sen. Aloizio Mercadante PT/SP 1 fevereiro de 2009 Evolução da Crise Fase 1 2001-2006: Bolha Imobiliária. Intensa liquidez. Abundância de crédito Inovações financeiras Elevação

O Brasil e a Crise Internacional Sen. Aloizio Mercadante PT/SP 1 fevereiro de 2009 Evolução da Crise Fase 1 2001-2006: Bolha Imobiliária. Intensa liquidez. Abundância de crédito Inovações financeiras Elevação